Introduction

California homeowners face a significant upfront decision when going solar: the average residential system costs roughly $21,400 before incentives, and most don't pay cash. The financing method you choose determines whether you profit substantially or merely break even over the system's 25-year lifespan — and the difference can run into the tens of thousands of dollars.

California's solar landscape is unlike any other state. Three factors make financing structure especially critical here:

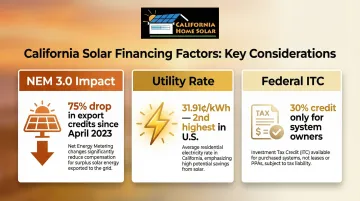

- NEM 3.0 slashed export credits by 75% as of April 2023, changing how much you earn back from excess generation

- Utility rates average 31.91 ¢/kWh — second-highest in the nation — meaning every kilowatt-hour you self-consume carries real dollar value

- The 30% federal tax credit goes only to system owners, not lessees

This guide breaks down the five main financing paths available to California homeowners — cash, loan, lease, PPA, and PACE — comparing ownership rights, tax credit eligibility, monthly costs, and long-term savings to help you identify the right fit for your situation.

TLDR

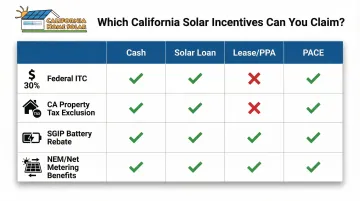

- Cash purchases deliver the highest lifetime savings and full access to the 30% federal tax credit

- Solar loans offer the same ownership benefits with $0 down — the most popular option for California homeowners

- Leases and PPAs have minimal upfront cost but forfeit the federal ITC and can complicate home sales

- PACE financing (including HERO) uses property-tax repayment with no credit score requirement, but places a lien on your home

- Under NEM 3.0, owning your system with battery storage yields significantly better returns than leasing or a PPA

Why Solar Financing Decisions Matter More in California Right Now

California's NEM 3.0, implemented in April 2023, reshaped solar economics across the state. The Net Billing Tariff cut surplus energy compensation from roughly 30 ¢/kWh to approximately 8 ¢/kWh — a 75% drop. Payback periods for solar-only systems stretched from 5–7 years to 8–10 years. That shift makes your financing structure the difference between strong returns and marginal ones.

Even so, solar remains a sound investment here. California's residential electricity rates sit at 31.91 ¢/kWh as of November 2025 — second only to Hawaii — which means every kilowatt-hour you generate yourself has real dollar value. The wrong financing method, though, can quietly erase what would otherwise be thousands in savings.

The federal Residential Clean Energy Credit—currently 30% through 2032—is only available to system owners. Lessees and PPA customers forfeit this benefit entirely, transferring thousands of dollars in tax credits to the solar company instead of capturing them personally.

Before choosing how to finance, it helps to understand what's at stake across each option:

- Tax credit eligibility: The federal Residential Clean Energy Credit (30% through 2032) goes only to system owners — lessees and PPA customers transfer this benefit to the solar company

- Payback timeline: Loan and cash purchases now average 8–10 years under NEM 3.0; leases and PPAs shift that risk to the provider but cap your upside

- Long-term savings: Ownership builds equity; leases and PPAs lock in a contracted rate that may or may not beat future utility prices

The 5 Solar Financing Options in California, Compared

Each option works differently in terms of ownership, monthly costs, and which tax incentives you can claim. The right choice depends on your financial goals, credit profile, and how long you plan to stay in your home. Use the comparison table below as a quick reference.

Cash Purchase

Paying cash upfront eliminates interest costs and delivers the highest total lifetime savings. You own the system immediately, qualify for the 30% federal ITC, and can claim California's property tax exclusion and SGIP battery rebates.

Payback timeline: 5-7 years in California post-NEM 3.0, driven by high utility rates.

Main drawback: Large upfront capital requirement. A typical 9 kW system in Southern California costs approximately $21,400 before incentives (or $23,485 for a 10 kW system in Los Angeles). Best suited for homeowners with available savings who plan to stay 10+ years.

Solar Loan

Solar loans allow system ownership with $0 or low money down, paid through monthly installments. Because you own the system, you qualify for the 30% federal ITC—which can substantially reduce effective loan cost if applied to principal in year one.

Key variables to evaluate:

- Loan terms: Typically 10-25 years

- Interest rates: 6-12% APR for solar-specific loans, or 6-12% for home equity loans

- Credit requirements: Most lenders require a minimum 650 credit score, though some accept 580-600 with higher rates

- Dealer fees: Watch for origination fees of 1-5% added to principal, which inflate effective system cost

Strategy: Apply your ITC refund toward the loan principal in year one to lower monthly payments and reduce total interest paid.

Solar Lease

A solar lease means you pay a fixed monthly fee to use panels installed by a third-party company. The company owns the panels, handles maintenance, and you do not qualify for the federal ITC or state ownership-based incentives. Monthly payments are typically lower than loans, but savings accumulate more slowly.

California-specific concerns:

- Annual escalators: Lease payments typically increase 1-3% annually, meaning costs rise each year

- Home sale complications: The lease must be transferred to the buyer, which can delay or derail real estate transactions—transfers require credit checks on purchasers

- Under NEM 3.0: The savings advantage of leasing has narrowed significantly compared to ownership

Power Purchase Agreement (PPA)

A PPA differs from a lease: you pay per kilowatt-hour consumed from the panels (rather than a flat monthly fee) at a rate lower than the utility's rate. The third-party company owns, installs, and maintains the system. There's no upfront cost, but you also won't qualify for the federal ITC or build any ownership equity.

Current rates: Southern California residential PPA rates range from $0.12-$0.16/kWh (2025), compared to SCE's average rate of approximately 35.3 ¢/kWh. LADWP's standard residential rates are lower, around 20-23 ¢/kWh.

Important considerations:

- PPA rates often include 1-3% annual escalators

- Contracts typically run 20-25 years

- Like leases, PPAs complicate home sales and lock you into those multi-decade contracts

- Under NEM 3.0, ownership with battery storage now delivers stronger long-term value than a PPA for most Southern California homeowners

PACE Financing (Including HERO Program)

Property Assessed Clean Energy (PACE) financing is unique to California. It lets homeowners fund solar through their property tax bill, with no separate monthly loan payment and no traditional credit score requirement. PACE financing places a lien on your property; repayment spans 10-30 years, and you retain system ownership (and federal ITC eligibility).

Key features:

- Administrators: California has multiple state-licensed PACE administrators including Ygrene, Renew Financial (CaliforniaFIRST), and HERO

- Qualification: Based on property equity and mortgage payment history, not FICO score

- Repayment: Billed as a line item on your property tax bill

CA Home Solar is a HERO Registered Contractor, so Los Angeles-area homeowners can use PACE financing directly through us — no need to source a separate contractor.

Risks to understand:

- PACE loans carry higher interest rates than traditional solar loans (6-12% APR)

- The lien creates a super-priority claim that can complicate refinancing or selling—Fannie Mae and Freddie Mac generally prohibit purchasing mortgages with outstanding PACE liens

- Best suited for homeowners who lack the credit profile for traditional solar loans but want ownership benefits

Comparison Table: All 5 Options at a Glance

| Feature | Cash | Solar Loan | Lease | PPA | PACE |

|---|---|---|---|---|---|

| Upfront Cost | $21,000-$24,000 | $0-$1,000 | $0 | $0 | $0 |

| Monthly Payment | None | $100-$250 | $50-$150 | Varies by usage | None (property tax) |

| System Ownership | Yes | Yes | No | No | Yes |

| Eligible for 30% Federal ITC | Yes | Yes | No | No | Yes |

| Eligible for SGIP/State Incentives | Yes | Yes | No | No | Yes |

| Maintenance Responsibility | Homeowner | Homeowner | Solar company | Solar company | Homeowner |

| Home Sale Complexity | Low | Low | High | High | Medium-High |

| Best For | High savings, long-term owners | Ownership without depleting savings | Low/no tax liability, short-term owners | Predictable per-kWh costs | Poor credit, want ownership |

Which Solar Financing Option Is Right for You?

The right choice depends on four key variables: available cash/capital, federal tax liability, credit score and debt-to-income ratio, and how long you plan to stay in the home.

Federal tax liability matters: You need to owe taxes to benefit from the ITC. If your tax liability is less than the credit amount, you can carry forward unused portions, but the benefit is delayed.

The profiles below map each financing type to the homeowner it fits best — starting with ownership options, then alternatives for those who can't or don't want to own.

Ideal cash buyer profile:

- Has $20,000+ available

- Significant federal tax liability

- Plans to stay 10+ years

- Wants maximum lifetime ROI

The 30% federal ITC dramatically accelerates payback—for a $21,400 system, that's $6,420 back in tax credits, reducing net cost to roughly $15,000.

Ideal solar loan profile:

- Good credit (typically 650+ minimum)

- Has federal tax liability to use the ITC

- Wants ownership benefits without depleting savings

- Can apply ITC payment to loan principal in year one

This is the most common financing path for Southern California homeowners and yields strong returns, especially when the ITC payment reduces the loan balance.

When a lease or PPA makes sense:

- Low or no federal tax liability (retired, lower income)

- Don't want maintenance responsibility

- Plan to sell within a few years and want simplicity

Even then, lease transfer complications exist. Under NEM 3.0, the savings gap between leasing and owning has widened considerably — ownership now delivers stronger long-term returns in most California scenarios.

If neither ownership nor leasing fits your situation, PACE financing offers a middle path.

When PACE makes sense:

- Can't qualify for traditional loan due to credit challenges

- Want ownership benefits and ITC eligibility

- Prefer property-tax-based repayment

- Have significant equity and no immediate plans to refinance or sell

A solar installer familiar with PACE programs — like CA Home Solar, which is a HERO Registered Contractor — can help you determine whether your equity position and financial timeline make it a viable fit.

California-Specific Incentives and What Each Financing Option Qualifies For

Not every incentive is available to every financing type. Here's how California's key programs line up against cash, loan, lease, and PPA options.

Federal Residential Clean Energy Credit (ITC) — only cash buyers and loan customers qualify. Because you must own the system to claim it, lessees and PPA customers are excluded; the third-party owner takes the credit instead.

For a typical California system priced at $21,392, the 30% credit saves roughly $6,417. The rate holds at 30% through 2032, then steps down to 26% in 2033 and 22% in 2034 before expiring — so timing your purchase matters.

California property tax exclusion applies to system owners (cash, loan, PACE) — not leased systems. Under state law, the added value of a solar installation is excluded from property tax assessment, so your tax bill won't climb after installation.

Self-Generation Incentive Program (SGIP) offers rebates for battery storage to system owners. Post-NEM 3.0, storing excess energy for peak-hour use is far more valuable than exporting it at reduced rates — making battery pairing a practical move for loan and cash buyers. Note that as of 2025, most SGIP funds are reserved for equity and low-income budgets.

Los Angeles-Area Details

Two local factors affect how these incentives play out in Southern California:

- LADWP customers operate outside NEM 3.0. The utility runs its own net metering program that typically credits excess generation more favorably than SCE customers see under NEM 3.0.

- Community solar is available through Clean Power Alliance for homeowners who can't install rooftop panels — qualifying households in disadvantaged communities can access 20% electric bill discounts.

Conclusion

For most Southern California homeowners, a solar loan offers the best balance of ownership benefits, tax credit access, and affordability—but the right answer depends on your financial profile and how long you plan to stay in the property.

With NEM 3.0 in place, owning your system and pairing it with battery storage is the strategy that maximizes long-term savings in California. Choosing the wrong financing structure can undercut what would otherwise be a strong investment, potentially costing you thousands in forfeited tax credits and reduced lifetime savings.

That's where working with an experienced local installer makes a real difference. CA Home Solar has served Southern California homeowners for 36 years and holds recognition as a Top 500 Solar Contractor. The team helps Los Angeles-area homeowners navigate all available financing options—including PACE/HERO programs—to find the right fit for their situation, property, and goals.

Call 877-903-1012 or email info@cahomesolar.com to schedule a personalized consultation.

Frequently Asked Questions

Is financing solar a good idea in California?

Financing solar in California (particularly via a solar loan) remains a strong financial decision because the 30% federal ITC, California's high utility rates, and the property tax exclusion combine to offset costs. Though NEM 3.0 has extended payback timelines to 8-10 years, the right financing structure preserves substantial long-term value.

Is it better to lease, buy, or sign a PPA for solar in California?

Buying (via cash or loan) is generally better in California because it qualifies for the 30% federal ITC and SGIP battery incentives. Ownership has become more advantageous under NEM 3.0. Leases and PPAs make sense primarily for homeowners with no federal tax liability or those who prefer zero maintenance responsibility.

Are free or zero-down solar options worth it in California?

"Free" or $0-down solar options involve real trade-offs: PPAs and leases forfeit the federal ITC and may bring escalating payments or home-sale complications. $0-down solar loans preserve ownership benefits and are generally the better zero-upfront-cost option for most California homeowners.

What is PACE financing in California and how does it compare to other solar financing options?

PACE financing lets California homeowners repay solar costs through their property tax bill, requires no minimum credit score, and preserves ownership for ITC eligibility. The trade-offs: higher interest rates (6-12% APR) than solar loans and a super-priority lien that can complicate refinancing or home sales.

What are the 20%, 30%, and 33% rules or credits related to solar in California?

The federal Residential Clean Energy Credit is currently 30% (through 2032), drops to 26% in 2033 and 22% in 2034 before expiring. This is a tax credit (not a rebate), only available to system owners, applied against federal income tax liability—lessees and PPA customers cannot claim it.

Will NEM 3.0 be overturned in California?

NEM 3.0 remains in effect as of 2025 — no formal reversal has been enacted, though advocacy groups continue to challenge it in court. Plan your financing around current NEM 3.0 rules; battery storage is the primary strategy to maximize solar value under the new framework.